Applications for the LAMP Fellowship 2025-26 will open on December 1, 2024. Sign up here to be notified. Last date for submitting the applications is December 21, 2024.

The central government has enforced a nation-wide lockdown between March 25 and May 3 as part of its measures to contain the spread of COVID-19. During the lockdown, several restrictions have been placed on the movement of individuals and economic activities have come to a halt barring the activities related to essential goods and services. The restrictions are being relaxed in less affected areas in a limited manner since April 20. In this blog, we look at how the lockdown has impacted the demand and supply of electricity and what possible repercussions its prolonged effect may have on the power sector.

Power supply saw a decrease of 25% during the lockdown (year-on-year)

As electricity cannot be stored in large amount, the power generation and supply for a given day are planned based on the forecast for demand. The months of January and February in 2020 had seen an increase of 3% and 7% in power supply, respectively as compared to 2019 (year-on-year). In comparison, the power supply saw a decrease of 3% between March 1 and March 24. During the lockdown between March 24 and April 19, the total power supply saw a decrease of about 25% (year-on-year).

Figure 1: % change in power supply position between March 1 and April 19 (Y-o-Y from 2019 to 2020)

Sources: Daily Reports; POSOCO; PRS.

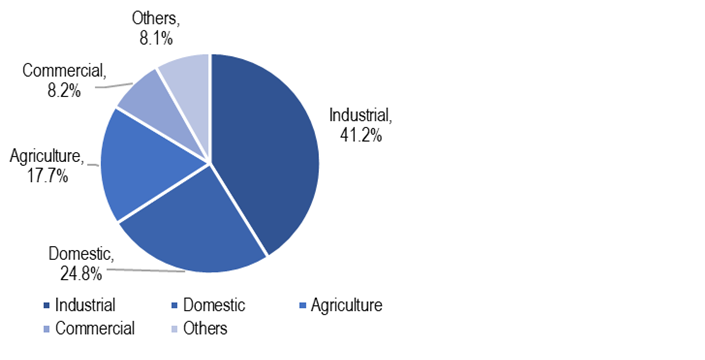

If we look at the consumption pattern by consumer category, in 2018-19, 41% of total electricity consumption was for industrial purposes, followed by 25% for domestic and 18% for agricultural purposes. As the lockdown has severely reduced the industrial and commercial activities in the country, these segments would have seen a considerable decline in demand for electricity. However, note that the domestic demand may have seen an uptick as people are staying indoors.

Figure 2: Power consumption by consumer segment in 2018-19

Sources: Central Electricity Authority; PRS.

Electricity demand may continue to be subdued over the next few months. At this point, it is unclear that when lockdown restrictions are eased, how soon will economic activities return to pre COVID-19 levels. India’s growth projections also highlight a slowdown in the economy in 2020 which will further impact the demand for electricity. On April 16, the International Monetary Fund has slashed its projection for India’s GDP growth in 2020 from 5.8% to 1.9%.

A nominal increase in energy and peak deficit levels

As power sector related operations have been classified as essential services, the plant operations and availability of fuel (primarily coal) have not been significantly constrained. This can be observed with the energy deficit and peak deficit levels during the lockdown period which have remained at a nominal level. Energy deficit indicates the shortfall in energy supply against the demand during the day. The average energy deficit between March 25 and April 19 has been 0.42% while the corresponding figure was 0.33% between March 1 and March 24. Similarly, the average peak deficit between March 25 and April 19 has been 0.56% as compared to 0.41% between March 1 and March 24. Peak deficit indicates the shortfall in supply against demand during highest consumption period in a day.

Figure 3: Energy deficit and peak deficit between March 1, 2020 and April 19, 2020 (in %)

Sources: Daily Reports; POSOCO; PRS.

Coal stock with power plants increases

Coal is the primary source of power generation in the country (~71% in March 2020). During the lockdown period, the coal stock with coal power plants has seen an increase. As of April 19, total coal-stock with the power plants in the country (in days) has risen to 29 days as compared to 24 days on March 24. This indicates that the supply of coal has not been constrained during the lockdown, at least to the extent of meeting the requirements of power plants.

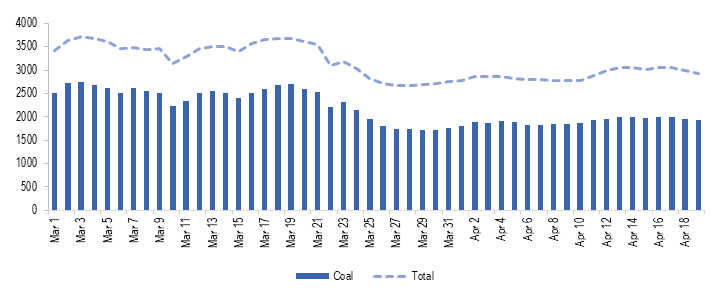

Energy mix changes during the lockdown, power generation from coal impacted

During the lockdown, power generation has been adjusted to compensate for reduced consumption, Most of this reduction in consumption has been adjusted by reduced coal power generation. As can be seen in Table 1, coal power generation reduced from an average of 2,511 MU between March 1 and March 24 to 1,873 MU between March 25 and April 19 (about 25%). As a result, the contribution of coal in total power generation reduced from an average of 72.5% to 65.6% between these two periods.

Table 1: Energy Mix during March 1-April 19, 2020

Sources: Daily Reports; POSOCO; PRS.

This shift may be happening due to various reasons including: (i) renewable energy sources (solar, wind, and small hydro) have MUST RUN status, i.e., the power generated by them has to be given the highest priority by distribution companies, and (ii) running cost of renewable power plants is lower as compared to thermal power plants.

This suggests that if growth in electricity demand were to remain weak, the adverse impact on the coal power plants could be more as compared to other power generation sources. This will also translate into weak demand for coal in the country as almost 87% of the domestic coal production is used by the power sector. Note that the plant load factor (PLF) of the thermal power plants has seen a considerable decline over the years, decreasing from 77.5% in 2009-10 to 56.4% in 2019-20. Low PLF implies that coal plants have been lying idle. Coal power plants require significant fixed costs, and they incur such costs even when the plant is lying idle. The declining capacity utilisation augmented by a weaker demand will undermine the financial viability of these plants further.

Figure 4: Power generation from coal between March 1, 2020 and April 19, 2020 (in MU)

Sources: Daily Reports; POSOCO; PRS.

Finances of the power sector to be severely impacted

Power distribution companies (discoms) buy power from generation companies and supply it to consumers. In India, most of the discoms are state-owned utilities. One of the key concerns in the Indian power sector has been the poor financial health of its discoms. The discoms have had high levels of debt and have been running losses. The debt problem was partly addressed under the UDAY scheme as state governments took over 75% of the debt of state-run discoms (around 2.1 lakh crore in two years 2015-16 and 2016-17). However, discoms have continued to register losses owing to underpricing of electricity tariff for some consumer segments, and other forms of technical and commercial losses. Outstanding dues of discoms towards power generation companies have also been increasing, indicating financial stress in some discoms. At the end of February 2020, the total outstanding dues of discoms to generation companies stood at Rs 92,602 crore.

Due to the lockdown and its further impact in the near term, the financial situation of discoms is likely to be aggravated. This will also impact other entities in the value chain including generation companies and their fuel suppliers. This may lead to reduced availability of working capital for these entities and an increase in the risk of NPAs in the sector. Note that, as of February 2020, the power sector has the largest share in the deployment of domestic bank credit among industries (Rs 5.4 lakh crore, 19.3% of total).

Following are some of the factors which have impacted the financial situation during the lockdown:

Reduced cross-subsidy: In most states, the electricity tariff for domestic and agriculture consumers is lower than the actual cost of supply. Along with the subsidy by the state governments, this gap in revenue is partly compensated by charging industrial and commercial consumers at a higher rate. Hence, industrial and commercial segments cross-subsidise the power consumption by domestic and agricultural consumers.

The lockdown has led to a halt on commercial and industrial activities while people are staying indoors. This has led to a situation where the demand from the consumer segments who cross-subsidise has decreased while the demand from consumer segments who are cross-subsidised has increased. Due to this, the gap between revenue realised by discoms and cost of supply will widen, leading to further losses for discoms. States may choose to bridge this gap by providing a higher subsidy.

Moratorium to consumers: To mitigate the financial hardship of citizens due to COVID-19, some states such as Rajasthan, Uttar Pradesh, and Goa, among others, have provided consumers with a moratorium for payment of electricity bills. At the same time, the discoms are required to continue supplying electricity. This will mean that the return for the supply made in March and April will be delayed, leading to lesser cash in hand for discoms.

Some state governments such as Bihar also announced a reduction in tariff for domestic and agricultural consumers. Although, the reduction in tariff will be compensated to discoms by government subsidy.

Constraints with government finances: The revenue collection of states has been severely impacted as economic activities have come to a halt. Further, the state governments are directing their resources for funding relief measures such as food distribution, direct cash transfers, and healthcare. This may adversely affect or delay the subsidy transfer to discoms.

The UDAY scheme also requires states to progressively fund greater share in losses of discoms from their budgetary resources (10% in 2018-19, 25% in 2019-20, and 50% in 2020-21). As losses of discoms may widen due to the above-mentioned factors, the state government’s financial burden is likely to increase.

Capacity addition may be adversely impacted

As per the National Electricity Plan, India’s total capacity addition target is around 176 GW for 2017-2022. This comprises of 118 GW from renewable sources, 6.8 GW from hydro sources, and 6.4 GW from coal (apart from 47.8 GW of coal-based power projects already in various stages of production as of January 2018).

India has set a goal of installing 175 GW of Renewable Power Capacity by 2022 as part of its climate change commitments (86 GW has been installed as of January 2020). In January 2020, the Parliamentary Standing Committee on Energy observed that India could only install 82% and 55% of its annual renewable energy capacity addition targets in 2017-18 and 2018-19. As of January 2020, 67% of the target has been achieved for 2019-20.

Due to the impact of COVID-19, the capacity addition targets for various sources is likely to be adversely impacted in the short run as:

construction activities were stopped during the lockdown and will take some time to return to normal,

disruption in the global supply chain may lead to difficulties with the availability of key components leading to delay in execution of projects, for instance, for solar power plants, solar PV modules are mainly imported from China, and

reduced revenue for companies due to weak demand will leave companies with less capacity left for capital expenditure.

Key reforms likely to be delayed

Following are some of the important reforms anticipated in 2020-21 which may get delayed due to the developing situation:

The real-time market for electricity: The real-time market for electricity was to be operationalised from April 1, 2020. However, the lockdown has led to delay in completion of testing and trial runs. The revised date for implementation is now June 1, 2020.

UDAY 2.0/ADITYA: A new scheme for the financial turnaround of discoms was likely to come this year. The scheme would have provided for the installation of smart meters and incentives for rationalisation of the tariff, among other things. It remains to be seen what this scheme would be like since the situation with government finances is also going to worsen due to anticipated economic slowdown.

Auction of coal blocks for commercial mining: The Coal Ministry has been considering auction of coal mines for commercial mining this year. 100% FDI has been allowed in the coal mining activity for commercial sale of coal to attract foreign players. However, the global economic slowdown may mean that the auctions may not generate enough interest from foreign as well as domestic players.

For a detailed analysis of the Indian Power Sector, please see here. For details on the number of daily COVID-19 cases in the country and across states, please see here. For details on the major COVID-19 related notifications released by the centre and the states, please see here.

TRAI released its recommendations on auction of spectrum on April 23, 2012. The recommendations are in pursuance of the Supreme Court order cancelling 122 telecom licences. The cancellation was ordered on grounds of procedural irregularities and arbitrariness in the first-cum-first-serve policy for allocation of spectrum. The recommendations, if adopted by the Department of Telecommunications, would change various aspects of the present telecom policy, including (a) relationship between a telecom licence and spectrum; (b) procedure for allocation of spectrum; (c) pricing of spectrum; (d) limits on spectrum allocation; and (e) use of spectrum. Relationship between telecom licences and spectrum Previously, under the Telecom Policy 1994 (updated in 1999), spectrum was tied in with telecom licences. Since 2003, licence conditions provided for award of two blocks of 6.2 MHz of spectrum for GSM technology and two blocks of 5 MHz for CDMA technology. As per the government’s decision of January 17, 2008 (as explained in TRAI's consultation paper, see page 3 paragraph 7) additional spectrum would be awarded on the basis of increment in the number of subscribers. Service providers had to pay a licence fee (on obtaining the licence), an annual licence fee and a spectrum usage charge determined on the basis of their adjusted gross revenue. TRAI has recommended that telecom licences and spectrum should be de-linked. The service provider would thus pay separately for the value of the licence and the spectrum. With this formulation an entity that does not hold a licence, but is eligible to secure one, may also procure spectrum. This would help in avoiding situations where licence holders have to wait to secure spectrum or offer wire line services in the absence of spectrum. Procedure for allocation of spectrum TRAI has recommended that spectrum be auctioned by means of a simultaneous multiple round ascending auction (SMRA). This means that the service providers would bid for spectrum in different blocks simultaneously. In the first round of auction a reserve price (base price) set by the government is used. Reserve price for auction and payment mechanism A reserve price indicates the minimum amount the bidder must pay to win the object. In case it is too low, it may reduce the gains made by the seller and lead to a sub-optimal sale. If it is too high, it may reduce the number of bidders and the probability of the good not being sold. Various countries have adopted a reserve price of 0.5 times the final price. TRAI has recommended that the reserve price should be 0.8 times the expected winning bid. It has also recommended that telecom companies pay 67% to 75% of the final price in installments over 10 years, depending on the spectrum band. TRAI has reasoned that a higher price would reduce the possibility of further sales upon bidders securing spectrum. However, this may lead to fewer bidders and ultimately fewer service providers. It is argued in news reports that this may increase investments to be made by the service providers and eventually an increase in tariffs. Spectrum blocks and caps TRAI has recommended that the spectrum cap should be determined on the basis of market share. A service provider can now secure a maximum of 50% of spectrum assigned in each band in each service area. However, a service provider cannot hold more than 25% of the total spectrum assigned in all the bands across the country. As per the January 2008 decision, additional spectrum could be awarded to telecom companies when they reached incremental slabs of subscribers. This could extend to two blocks of 1 MHz for GSM technology, and two blocks of 1.25 MHz for CDMA, for each slab of subscribers. TRAI has recommended that spectrum should be auctioned in blocks of 1.25 MHz. Each auction would at least offer 5 MHz of spectrum at a time. Smaller blocks would ensure that service providers who are nearing the spectrum cap may secure spectrum without exceeding the cap. However, experts have argued that 1.25 MHz block may be too limited for launching services. Also, TRAI in the recommendation has noted that a minimum of 5 MHz of contiguous spectrum is required to launch efficient services with new technologies. Use of spectrum TRAI has recommended that the use of spectrum should be liberalised. This implies that spectrum should be technology neutral. Telecom companies would now be free to launch services with any technology of their choice.