Applications for the LAMP Fellowship 2025-26 will open on December 1, 2024. Sign up here to be notified. Last date for submitting the applications is December 21, 2024.

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

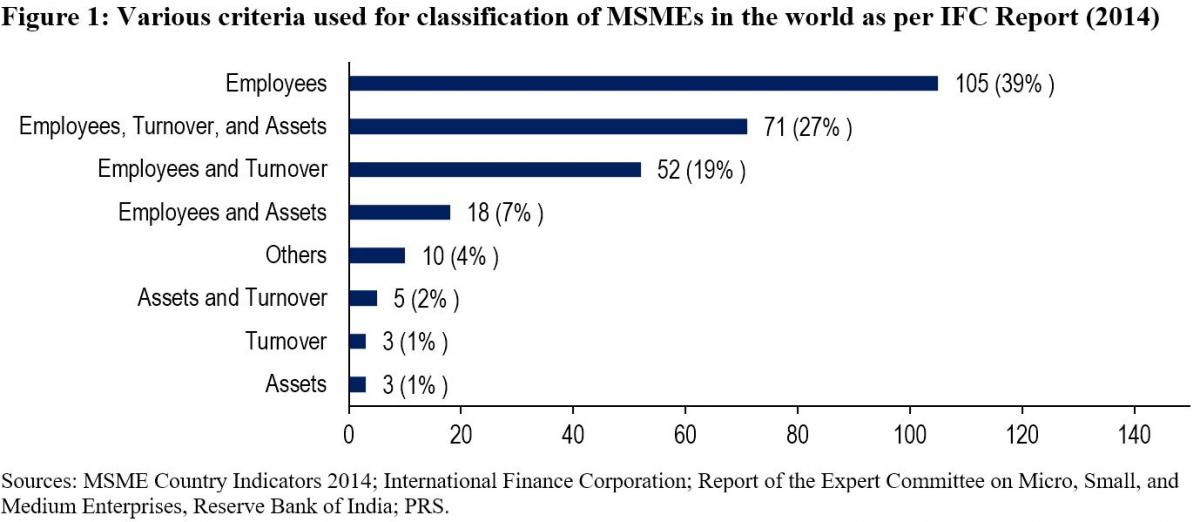

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

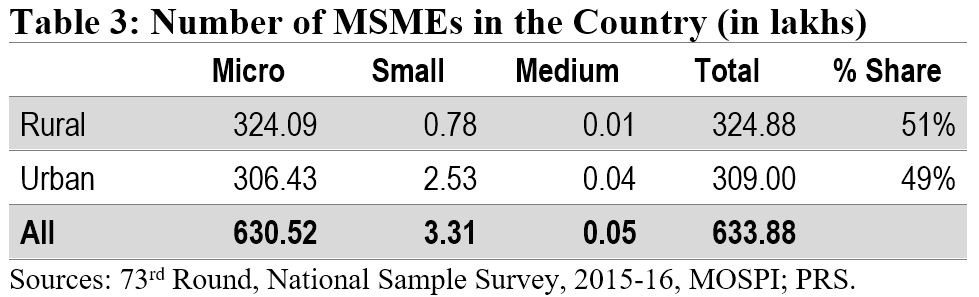

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

Employment in the MSME sector

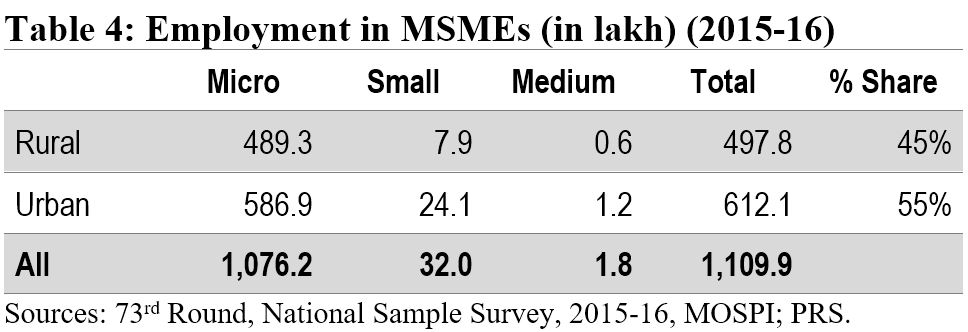

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.

In the past few months, retail prices of petrol and diesel have consistently increased and have reached all-time high levels. On September 24, 2018, the retail price of petrol in Delhi was Rs 82.72/litre, and that of diesel was Rs 74.02/litre. In Mumbai, these prices were even higher at Rs 90.08/litre and Rs 78.58/litre, respectively.

The difference in retail prices in the two cities is because of the different tax rates levied by the respective state governments on the same products. This blog post explains the major tax components in the price structure of petrol and diesel and how tax rates vary across states. It also analyses the shift in the taxation of these products, its effect on retail prices, and the consequent revenue generated by the central and state governments.

What are the components of the price structure of petrol and diesel?

Retail prices of petrol and diesel in India are revised by oil companies on a daily basis, according to changes in the price of global crude oil. However, the price paid by oil companies makes up 51% of the retail price in case of petrol, and 61% in the case of diesel (Table 1). The break-up of retail prices of petrol and diesel in Delhi, as on September 24, 2018, shows that over 45% of the retail price of petrol comprises central and states taxes. In the case of diesel, this is close to 36%.

At present, the central government has the power to tax the production of petroleum products, while states have the power to tax their sale. The central government levies an excise duty of Rs 19.5/litre on petrol and Rs 15.3/litre on diesel. These make up 24% and 21% of the retail prices of petrol and diesel, respectively.

While excise duty rates are uniform across the country, states levy sales tax/value added tax (VAT), the rates of which differ across states. The figure below shows the different tax rates levied by states on petrol and diesel, which results in their varying retail prices across the country. For instance, the tax rates levied by states on petrol ranges from 17% in Goa to 39% in Maharashtra.

Note that unlike excise duty, sales tax is an ad valorem tax, i.e., it does not have a fixed value, and is charged as a percentage of the price of the product. This implies that while the excise duty component of the price structure is fixed, the sales tax component is charged as a proportion of the price paid by oil companies, which in turn depends on the global crude oil price. With the recent increase in the global prices, and subsequently the retail prices, some states such as Rajasthan, Andhra Pradesh, West Bengal, and Karnataka have announced tax rate cuts.

How have retail prices in India changed vis-à-vis the global crude oil price?

India’s dependence on imports for consumption of petroleum products has increased over the years. For instance, in 1998-99, net imports were 69% of the total consumption, which increased to 93% in 2017-18. Because of a large share of imports in the domestic consumption, any change in the global price of crude oil has a significant impact on the domestic prices of petroleum products. The following figures show the trend in price of global crude oil and retail price of petrol and diesel in India, over the last six years.

The global price of crude oil (Indian basket) decreased from USD 112/barrel in September 2012 to USD 28/barrel in January 2016. Though the global price dropped by 75% during this period, retail prices of petrol and diesel in India decreased only by 13% and 5%, respectively. This disparity in decrease of global and Indian retail prices was because of increase in taxes levied on petrol and diesel, which nullified the benefit of the sharp decline in the global price. Between October 2014and June 2016, the excise duty on petrol increased from Rs 11.02/litre to Rs 21.48/litre. In the same period, the excise duty on diesel increased from Rs 5.11/litre to Rs 17.33/litre.

Over the years, the central government has used taxes to prevent sharp fluctuations in the retail price of diesel and petrol. For instance, in the past, when global crude oil price has increased, duties have been cut. Since January 2016, the global crude oil price has increased by 158% from USD 28/barrel to USD 73/barrel in August 2018. However, during this period, excise duty has been reduced only once by Rs 2/litre in October 2017. While the central government has not signalled any excise duty cut so far, it remains to be seen if any rate cut will happen in case the global crude oil price rises further. With US economic sanctions on Iran coming into effect on November 4, 2018, India may face a shortfall in supply since Iran is India’s third largest oil supplier. Moreover, Organization of Petroleum Exporting Countries (OPEC) and Russia have not indicated any increase in supply from their side yet to offset the possible effect of sanctions. As a result, in a scenario with no tax rate cut, this could increase the retail prices of petrol and diesel even further.

How has the revenue generated from taxing petroleum products changed over the years?

As a result of successive increases in excise duty between November 2014 and January 2016, the year-on-year growth rate of excise duty collections increased from 27% in 2014-15 to 80% in 2015-16. In comparison, the growth rate of sales tax collections was 6% in 2014-15 and 4% in 2015-16. The figure below shows the tax collections from the levy of excise duty and sales tax on petroleum products. From 2011-12 to 2017-18, excise duty and sales tax collections grew annually at a rate of 22% and 11%, respectively.

How is this revenue shared between centre and states?

Though central taxes are levied by the centre, it gets only 58% of the revenue from the levy of these taxes. The rest 42% is devolved to the states as per the recommendations of the 14th Finance Commission. However, excise duty levied on petrol and diesel consists of two broad components – (i) excise duty component, and (ii) road and infrastructure cess. Of this, only the revenue generated from the excise duty component is devolved to states. Revenue generated by the centre from any cess is not devolved to states.

The cess component was increased by Rs 2/litre to Rs 8/litre in the Union Budget 2018-19. However, this was done by reducing the excise duty component by the same amount, so as to keep the overall rate the same. Essentially this provision shifted the revenue of Rs 2/litre of petrol and diesel from states’ divisible pool of taxes to the cess revenue, which is entirely with the centre. This cess revenue is earmarked for financing infrastructure projects.

At present, of the Rs 19.5/litre excise duty levied on petrol, Rs 11.5/litre is the duty component, and Rs 8/litre is the cess component. Therefore, accounting for 42% share of states in the duty component, centre effectively gets a revenue of Rs 14.7/litre, while states get Rs 4.8/litre. Similarly, excise duty of Rs 15.3/litre levied on diesel consists of a cess component of Rs 8/litre. Thus, excise duty on diesel effectively generates revenue of Rs 12.2/litre for the centre and Rs 3.1/litre for states.