Applications for the LAMP Fellowship 2025-26 will open on December 1, 2024. Sign up here to be notified when applications open.

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

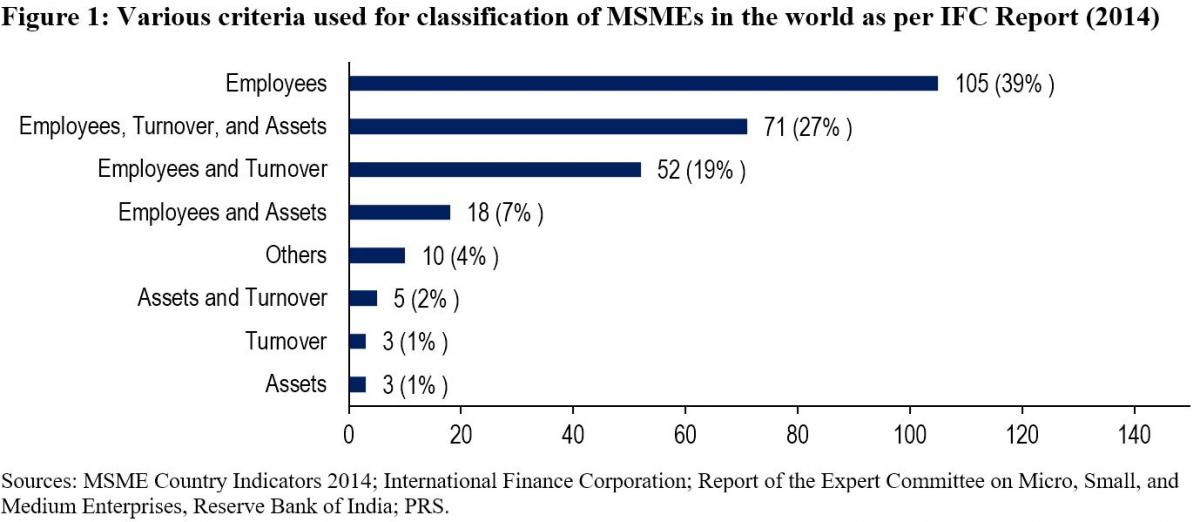

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

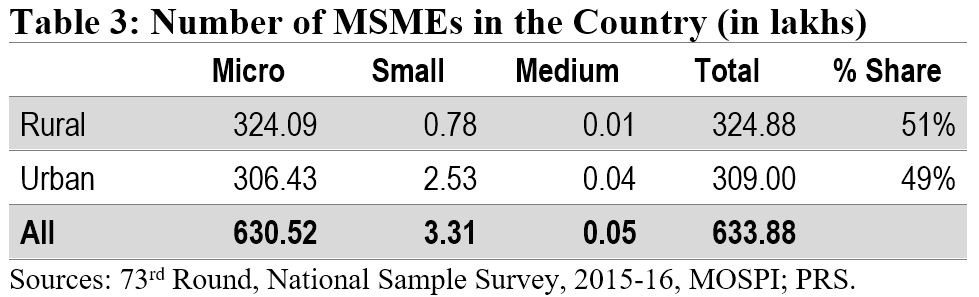

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

Employment in the MSME sector

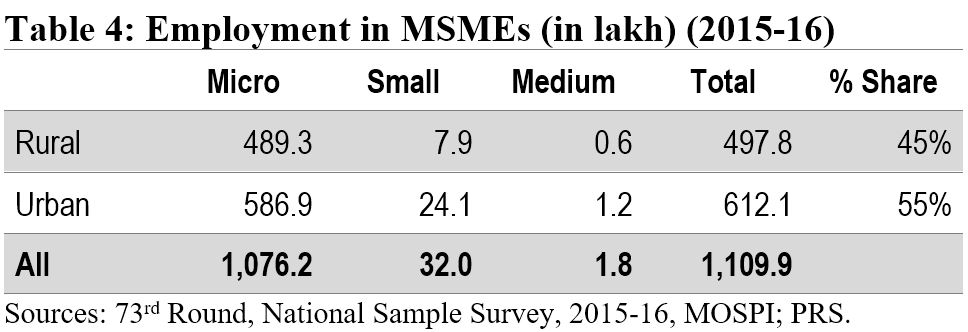

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.

Earlier this week, Lok Sabha passed the Bill that provides for the allocation of coal mines that were cancelled by the Supreme Court last year. In light of this development, this post looks at the issues surrounding coal block allocations and what the 2015 Bill seeks to achieve.

In September 2014, the Supreme Court cancelled the allocations of 204 coal blocks. Following the Supreme Court judgement, in October 2014, the government promulgated the Coal Mines (Special Provisions) Ordinance, 2014 for the allocation of the cancelled coal mines. The Ordinance, which was replaced by the Coal Mines (Special Provisions) Bill, 2014, could not be passed by Parliament in the last winter session, and lapsed. The government then promulgated the Coal Mines (Special Provisions) Second Ordinance, 2014 on December 26, 2014. The Coal Mines (Special Provisions) Bill, 2015 replaces the second Ordinance and was passed by Lok Sabha on March 4, 2015. Why is coal considered relevant? Coal mining in India has primarily been driven by the need for energy domestically. About 55% of the current commercial energy use is met by coal. The power sector is the major consumer of coal, using about 80% of domestically produced coal. As of April 1, 2014, India is estimated to have a cumulative total of 301.56 billion tonnes of coal reserves up to a depth of 1200 meters. Coal deposits are mainly located in Jharkhand, Odisha, Chhattisgarh, West Bengal, Madhya Pradesh, Andhra Pradesh and Maharashtra. How is coal regulated? The Ministry of Coal has the overall responsibility of managing coal reserves in the country. Coal India Limited, established in 1975, is a public sector undertaking, which looks at the production and marketing of coal in India. Currently, the sector is regulated by the ministry’s Coal Controller’s Organization. The Coal Mines (Nationalisation) Act, 1973 (CMN Act) is the primary legislation determining the eligibility for coal mining in India. The CMN Act allows private Indian companies to mine coal only for captive use. Captive mining is the coal mined for a specific end-use by the mine owner, but not for open sale in the market. End-uses currently allowed under the CMN Act include iron and steel production, generation of power, cement production and coal washing. The central government may notify additional end-uses. How were coal blocks allocated so far? Till 1993, there were no specific criteria for the allocation of captive coal blocks. Captive mining for coal was allowed in 1993 by amendments to the CMN Act. In 1993, a Screening Committee was set up by the Ministry of Coal to provide recommendations on allocations for captive coal mines. All allocations to private companies were made through the Screening Committee. For government companies, allocations for captive mining were made directly by the ministry. Certain coal blocks were allocated by the Ministry of Power for Ultra Mega Power Projects (UMPP) through tariff based competitive bidding (bidding for coal based on the tariff at which power is sold). Between 1993 and 2011, 218 coal blocks were allocated to both public and private companies under the CMN Act. What did the 2014 Supreme Court judgement do? In August 2012, the Comptroller and Auditor General of India released a report on the coal block allocations. CAG recommended that the allocation process should be made more transparent and objective, and done through competitive bidding. Following this report, in September 2012, a Public Interest Litigation matter was filed in the Supreme Court against the coal block allocations. The petition sought to cancel the allotment of the coal blocks in public interest on grounds that it was arbitrary, illegal and unconstitutional. In September 2014, the Supreme Court declared all allocations of coal blocks, made through the Screening Committee and through Government Dispensation route since 1993, as illegal. It cancelled the allocation of 204 out of 218 coal blocks. The allocations were deemed illegal on the grounds that: (i) the allocation procedure followed by the Screening Committee was arbitrary, and (ii) no objective criterion was used to determine the selection of companies. Further, the allocation procedure was held to be impermissible under the CMN Act. Among the 218 coal blocks, 40 were under production and six were ready to start production. Of the 40 blocks under production, 37 were cancelled and of the six ready to produce blocks, five were cancelled. However, the allocation to Ultra Mega Power Projects, which was done via competitive bidding for lowest tariffs, was not declared illegal. What does the 2015 Bill seek to do? Following the cancellation of the coal blocks, concerns were raised about further shortage in the supply of coal, resulting in more power supply disruptions. The 2015 Bill primarily seeks to allocate the coal mines that were declared illegal by the Supreme Court. It provides details for the auction process, compensation for the prior allottees, the process for transfer of mines and details of authorities that would conduct the auction. In December 2014, the ministry notified the Coal Mines (Special Provisions) Rules, 2014. The Rules provide further guidelines in relation to the eligibility and compensation for prior allottees. How is the allocation of coal blocks to be carried out through the 2015 Bill? The Bill creates three categories of mines, Schedule I, II and III. Schedule I consists of all the 204 mines that were cancelled by the Supreme Court. Of these mines, Schedule II consists of all the 42 mines that are under production and Schedule III consists of 32 mines that have a specified end-use such as power, iron and steel, cement and coal washing. Schedule I mines can be allocated by way of either public auction or allocation. For the public auction route any government, private or joint venture company can bid for the coal blocks. They can use the coal mined from these blocks for their own consumption, sale or for any other purpose as specified in their mining lease. The government may also choose to allot Schedule I mines to any government company or any company that was awarded a power plant project through competitive bidding. In such a case, a government company can use the coal mined for own consumption or sale. However, the Bill does not provide clarity on the purpose for which private companies can use the coal. Schedule II and III mines are to be allocated by way of public auction, and the auctions have to be completed by March 31, 2015. Any government company, private company or a joint venture with a specified end-use is eligible to bid for these mines. In addition, the Bill also provides details on authorities that would conduct the auction and allotment and the compensation for prior allottees. Prior allottees are not eligible to participate in the auction process if: (i) they have not paid the additional levy imposed by the Supreme Court; or (ii) if they are convicted of an offence related to coal block allocation and sentenced to imprisonment of more than three years. What are some of the issues to consider in the 2015 Bill? One of the major policy shifts the 2015 Bill seeks to achieve is to enable private companies to mine coal in the future, in order to improve the supply of coal in the market. Currently, the coal sector is regulated by the Coal Controller’s Organization, which is under the Ministry of Coal. The Bill does not establish an independent regulator to ensure a level playing field for both private and government companies bidding for auction of mines to conduct coal mining operations. In the past, when other sectors have opened up to the private sector, an independent regulatory body has been established beforehand. For example, the Telecom Regulatory Authority of India, an independent regulatory body, was established when the telecom sector was opened up for private service providers. The Bill also does not specify any guidelines on the monitoring of mining activities by the new allottees. While the Bill provides broad details of the process of auction and allotment, the actual results with regards to money coming in to the states, will depend more on specific details, such as the tender documents and floor price. It is also to be seen whether the new allotment process ensures equitable distribution of coal blocks among the companies and creates a fair, level-playing field for them. In the past, the functioning of coal mines has been delayed due to delays in land acquisition and environmental clearances. This Bill does not address these issues. The auctioning of coal blocks resulting in improving the supply of coal, and in turn addressing the problem of power shortage in the country, will also depend on the efficient functioning of the mines, in addition to factors such as transparent allocations.