Applications for the LAMP Fellowship 2025-26 will open on December 1, 2024. Sign up here to be notified when applications open.

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

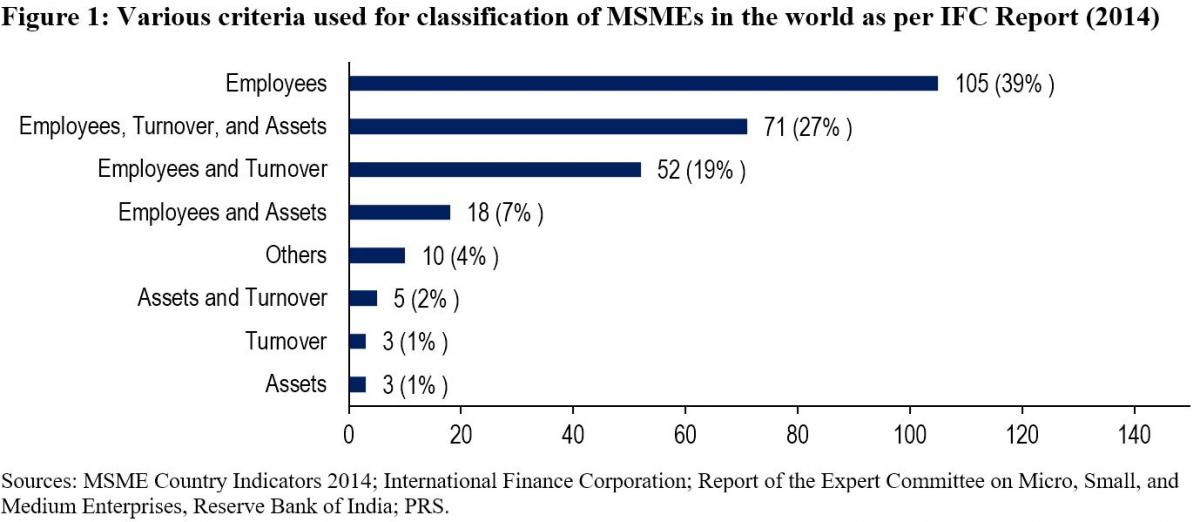

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

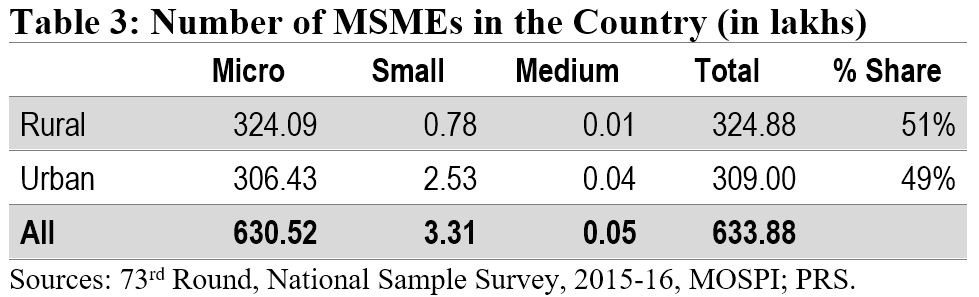

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

Employment in the MSME sector

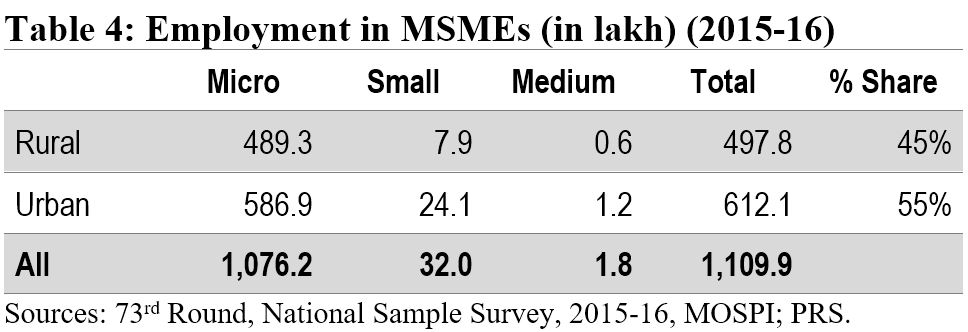

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.

The Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill, 2016 is listed for discussion in Rajya Sabha today.[i] The Bill aims to expeditiously resolve cases of debt recovery by making amendments to four laws, including the (i) Recovery of Debts Due to Banks and Financial Institutions Act, 1993, and (ii) the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. Recovery of Debts Due to Banks and Financial Institutions Act, 1993 The 1993 Act created Debt Recovery Tribunals (DRTS) to adjudicated debt recovery cases. This was done to move cases out of civil courts, with the idea of reducing time taken for debt recovery, and for providing technical expertise. This was aimed at assisting banks and financial institutions in recovering outstanding debt from defaulters. Over the years, it has been observed that the DRTs do not comply with the stipulated time frame of resolving disputes within six months. This has resulted in delays in disposal, and a high pendency of cases before the DRTs. Between March 2013 and December 2015, the number of pending cases before the DRTs increased from 43,000 to 70,000. With an average disposal rate of 10,000 cases per year, it is estimated that these DRTs will take about six to seven years to clear the existing backlog of cases.[ii] Experts have also observed that the DRT officers, responsible for debt recovery, lack experience in dealing with such cases. Further, these officers are not adequately trained to adjudicate debt-related matters.[iii] The 2016 Bill proposes to increase the retirement age of Presiding Officers of DRTs, and allows for their reappointment. This will allow the existing DRT officers to serve for longer periods of time. However, such a move may have limited impact in expanding the pool of officers in the DRTs. The 2016 Bill also has a provision which allows Presiding Officers of tribunals, established under other laws, to head DRTs. Currently, there are various specialised tribunals functioning in the country, like the Securities Appellate Tribunal, the National Company Law Tribunal, and theNational Green Tribunal. It remains to be seen if the skills brought in by officers of these tribunals will mirror the specialisation required for adjudicating debt-related matters. Further, the 1993 Act provides that banks and financial institutions must file cases in those DRTs that have jurisdiction over the defendant’s area of residence or business. In addition, the Bill allows cases to be filed in DRTs having jurisdiction over the bank branch where the debt is due. The Bill also provides that certain procedures, such as presentation of claims by parties and issue of summons by DRTs, can now be undertaken in electronic form (such as filing them on the DRT website). Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 The 2002 Act allows secured creditors (lenders whose loans are backed by a security) to take possession over a collateral security if the debtor defaults in repayment. This allows creditors to sell the collateral security and recover the outstanding debt without the intervention of a court or a tribunal. This takeover of collateral security is done with the assistance of the District Magistrate (DM), having jurisdiction over the security. Experts have noted that the absence of a time-limit for the DM to dispose such applications has resulted in delays.[iv] The 2016 Bill proposes to introduce a 30-day time limit within which the DM must pass an order for the takeover of a security. Under certain circumstances, this time-limit may be extended to 60 days. The 2002 Act also regulates the establishment and functioning of Asset Reconstruction Companies (ARCs). ARCs purchase Non-Performing Assets (NPAs) from banks at a discount. This allows banks to recover partial payment for an outstanding loan account, thereby helping them maintain cash flow and liquidity. The functioning of ARCs has been explained in Figure 1.  It has been observed that the setting up of ARCs, along with the use out-of-court systems to take possession of the collateral security, has created an environment conducive to lending.[iii] However, a few concerns related to the functioning of ARCs have been expressed over the years. These concerns include a limited number of buyers and capital entering the ARC business, and high transaction costs involved in the transfer of assets in favour of these companies due to the levy of stamp duty.[iii] In this regard, the Bill proposes to exempt the payment of stamp duty on transfer of financial assets in favour of ARCs. This benefit will not be applicable if the asset has been transferred for purposes other than securitisation or reconstruction (such as for the ARCs own use or investment). Consequently, the Bill amends the Indian Stamp Act, 1899. The Bill also provides greater powers to the Reserve Bank of India to regulate ARCs. This includes the power to carry out audits and inspections either on its own, or through specialised agencies. With the passage of the Bankruptcy Code in May 2016, a complete overhaul of the debt recovery proceedings was envisaged. The Code allows creditors to collectively take action against a defaulting debtor, and complete this process within a period of 180 days. During the process, the creditors may choose to revive a company by changing the repayment schedule of outstanding loans, or decide to sell it off for recovering their dues. While the Bankruptcy Code provides for collective action of creditors, the proposed amendments to the SARFAESI and DRT Acts seek to streamline the processes of creditors individually taking action against the defaulting debtor. The impact of these changes on debt recovery scenario in the country, and the issue of rising NPAs will only become clear in due course of time. [i] Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill, 2016, http://www.prsindia.org/administrator/uploads/media/Enforcement%20of%20Security/Enforcement%20of%20Security%20Bill,%202016.pdf. [ii] Unstarred Question No. 1570, Lok Sabha, Ministry of Finance, Answered on March 4, 2016. [iii] ‘A Hundred Small Steps’, Report of the Committee on Financial Sector Reforms, Planning Commission, September 2008, http://planningcommission.nic.in/reports/genrep/rep_fr/cfsr_all.pdf. [iv] Financial Sector Legislative Reforms Commission, March 2013, http://finmin.nic.in/fslrc/fslrc_report_vol1.pdf.

It has been observed that the setting up of ARCs, along with the use out-of-court systems to take possession of the collateral security, has created an environment conducive to lending.[iii] However, a few concerns related to the functioning of ARCs have been expressed over the years. These concerns include a limited number of buyers and capital entering the ARC business, and high transaction costs involved in the transfer of assets in favour of these companies due to the levy of stamp duty.[iii] In this regard, the Bill proposes to exempt the payment of stamp duty on transfer of financial assets in favour of ARCs. This benefit will not be applicable if the asset has been transferred for purposes other than securitisation or reconstruction (such as for the ARCs own use or investment). Consequently, the Bill amends the Indian Stamp Act, 1899. The Bill also provides greater powers to the Reserve Bank of India to regulate ARCs. This includes the power to carry out audits and inspections either on its own, or through specialised agencies. With the passage of the Bankruptcy Code in May 2016, a complete overhaul of the debt recovery proceedings was envisaged. The Code allows creditors to collectively take action against a defaulting debtor, and complete this process within a period of 180 days. During the process, the creditors may choose to revive a company by changing the repayment schedule of outstanding loans, or decide to sell it off for recovering their dues. While the Bankruptcy Code provides for collective action of creditors, the proposed amendments to the SARFAESI and DRT Acts seek to streamline the processes of creditors individually taking action against the defaulting debtor. The impact of these changes on debt recovery scenario in the country, and the issue of rising NPAs will only become clear in due course of time. [i] Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill, 2016, http://www.prsindia.org/administrator/uploads/media/Enforcement%20of%20Security/Enforcement%20of%20Security%20Bill,%202016.pdf. [ii] Unstarred Question No. 1570, Lok Sabha, Ministry of Finance, Answered on March 4, 2016. [iii] ‘A Hundred Small Steps’, Report of the Committee on Financial Sector Reforms, Planning Commission, September 2008, http://planningcommission.nic.in/reports/genrep/rep_fr/cfsr_all.pdf. [iv] Financial Sector Legislative Reforms Commission, March 2013, http://finmin.nic.in/fslrc/fslrc_report_vol1.pdf.